Australia is one of the countries with the highest cryptocurrency adoption rates globally. According to IRCI statistics, approximately 31% of Australian adults hold crypto assets in 2025, with Bitcoin investors accounting for 75%. Statista data predicts that cryptocurrency market revenue in Australia and Oceania will reach 1.4 billion USD in 2026, with an annual growth rate of about 19%. The popularization of crypto assets has brought about frequent cross-border and cross-platform transactions, making tax declarations more difficult and increasing the risk of hidden tax evasion. The tax compliance of crypto assets has gradually become a practical issue of universal social significance.

With the continuous expansion of the Australian crypto market, related tax treatment and regulatory application issues are becoming increasingly complex, and the traditional regulatory system falls short in the face of the emerging crypto asset sector. In April 2026, Australia passed the Corporations Amendment (Digital Assets Framework) Bill 2025, introducing the country's first comprehensive digital asset regulatory legislation. The bill officially takes effect 12 months from the date of Royal Assent, providing a certain transition period for industry entities to adapt to the new regulations. In terms of institutional design, the bill adopts a regulatory approach consistent with other jurisdictions such as Hong Kong, China, embedding digital assets into the existing financial licensing framework and regulating them by comparing their economic functions to those of traditional financial institutions.

Taking the recent regulatory reforms as an opportunity, this article conducts foundational research focusing on the crypto regulatory framework and tax treatment rules, analyzing how the emerging phenomenon of crypto assets is gradually integrating into Australia's financial and tax regulatory systems.

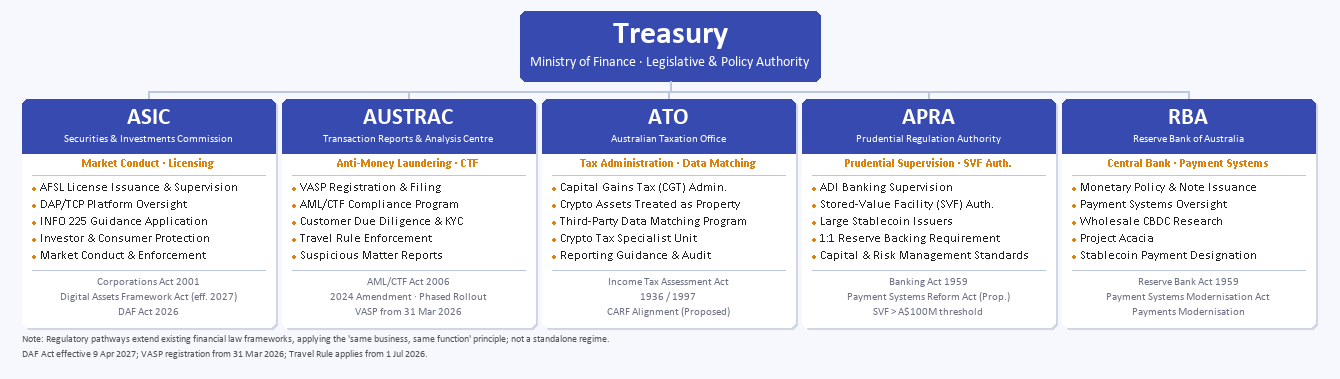

Current Australian regulation has not established a specialized regulatory body for crypto assets. Instead, based on the principle of same business and same rules, existing financial regulatory authorities manage them according to their respective functional divisions. For instance, the Australian Securities and Investments Commission (ASIC) is responsible for regulating crypto financial products and services, the Australian Transaction Reports and Analysis Centre (AUSTRAC) oversees anti-money laundering and counter-terrorism financing (AML/CTF) regulation, and the Australian Taxation Office (ATO) is responsible for tax collection and administration, taxing crypto assets according to relevant rules, and verifying declaration information through data matching programs with licensed exchanges.

Figure 1. Australia's Crypto Asset Regulatory Framework (Main Components)

According to Section 766A of the Corporations Act 2001, entities conducting financial services business in Australia must hold an Australian Financial Services Licence (AFSL), unless an exemption applies. ASIC states that the definitions of financial product and financial service under the existing Corporations Act 2001 can be applied based on the substantive characteristics of digital assets rather than their technical forms. Under current financial services laws, financial regulation is triggered only when the nature of a crypto asset is highly similar to traditional financial products. If a certain crypto asset fundamentally constitutes a security, a derivative, or a part of a managed investment scheme, the related issuance, trading, and advisory activities will fall within ASIC's scope of financial regulation. Conversely, for typical pure cryptocurrencies (such as BTC, ETH) and trading platforms not involving derivatives, they are generally not considered financial products or financial service providers, and relevant financial regulatory norms do not apply.

Under the Anti-Money Laundering and Counter-Terrorism Financing Act 2006, any enterprise providing digital currency exchange services must register with AUSTRAC as a digital currency exchange (DCE) provider. This registration system is designed to confirm that the enterprise's crypto trading business is authorized to operate in Australia and complies with Australia's AML/CTF framework and FATF international standards. In the DCE registration process, a comprehensive AML/CTF program is a core requirement for application, encompassing risk assessment, customer verification (KYC), employee training and internal controls, continuous transaction monitoring, and record keeping.

Relying solely on the existing financial services legal framework for regulation leads to a large number of crypto assets being difficult to classify, placing them in a regulatory grey area. The Corporations Amendment (Digital Assets Framework) Bill 2025 strengthens the regulation of crypto assets by defining new financial products and embedding trading platforms and custody services into the Australian Financial Services Licence (AFSL) system. The bill defines two new financial products: the Digital Asset Platform (DAP) and the Tokenized Custody Platform (TCP). A Digital Asset Platform (DAP) refers to a platform where an operator holds digital assets on behalf of clients and provides services such as transfer, trading, and staking, typical examples being cryptocurrency exchanges and custodial wallet services. A Tokenized Custody Platform (TCP) refers to a platform that tokenizes real-world assets (RWA) such as real estate, bonds, and commodities, and holds the underlying assets on behalf of clients. Essentially, the new regulations no longer focus on the similarity between the crypto assets themselves and financial products, but rather target the intermediary behavior of holding crypto assets on behalf of clients. Any platform holding crypto assets on behalf of clients, whether the underlying asset is Bitcoin or an RWA, must apply for an AFSL and fulfill the same level of obligations regarding client asset segregation, risk management, information disclosure, and even dispute resolution as brokers and fund managers.

The Australian Taxation Office (ATO) characterizes cryptocurrency as a CGT asset (Capital Gains Tax asset) rather than fiat currency. Depending on the specific transaction, cryptocurrency may also be considered additional income and taxed in the form of income tax.

The vast majority of crypto transactions, including selling, gifting, purchasing goods or services with cryptocurrency, and swapping between cryptocurrencies, constitute taxable disposal behaviors, triggering the calculation of capital gains or capital losses. Meanwhile, crypto yields obtained through methods such as staking, mining, and airdrops are treated as ordinary income under standard income tax rules, and are taxed at their fair market value upon receipt. As long as there is a transfer of asset ownership or economic benefit, it may constitute a disposal behavior, thereby triggering tax obligations. Conversely, purchasing cryptocurrency using Australian Dollars or other currencies, transferring between one's own wallets, and merely holding cryptocurrency without disposal, do not require tax payment.

In practice, the ATO further distinguishes the holding purposes and trading methods of investors to determine whether specific crypto asset activities fall within the scope of capital gains tax or ordinary income tax. The ATO clearly differentiates between two types of taxpayers: investors and traders, applying different tax treatment rules. If the purpose of holding coins is for medium-to-long-term holding and waiting for appreciation, and trading is infrequent, the individual belongs to the investor category, to which capital gains tax rules apply. If holding coins is for profit purposes, including engaging in high-frequency trading or arbitrage operations, conducting crypto asset mining or staking, and commercialized operations such as opening an exchange, the entity belongs to the trader category, to which ordinary income tax rules apply.

If cryptocurrency is owned as an investment, tax must be paid on the annual net capital gain. Capital gains need to be calculated as follows:

Capital Gain = Sales Price (Market Value) - Cost Base

Herein, the cost base refers to the amount paid to purchase the crypto asset (including transaction incidentals such as brokerage fees) and other incidental costs incurred to acquire the asset, including relevant expenditures such as the original purchase price, transfer fees, trading platform fees, and wallet custody fees. If crypto assets are held for more than 12 months, individual investors can enjoy a 50% capital gains tax discount. If a capital loss occurs, it can be used to offset other capital gains in the current year or carried forward to future years. However, if the cryptocurrency is a personal use asset and is purchased for 10,000 AUD or less, the capital gain generated from its disposal may be disregarded. Capital losses generated from personal use asset cryptocurrencies are also disregarded. If cryptocurrency is acquired and used for personal use or consumption (i.e., purchasing goods or services) within a short period, it is more likely to become a personal use asset.

If cryptocurrency is owned as a trade, the income must be included in ordinary income for tax payment, and it does not enjoy the capital gains tax discount. The income tax rate depends on the total income for that tax year.

| Income | Tax Rate |

|---|---|

| 0 - $18,200 | 0% |

| $18,201 - $45,000 | 16% |

| $45,001 - $135,000 | 30% |

| $135,001 - $190,000 | 37% |

| $190,001 and above | 45% |

Table 1. Australia's 2025-2026 Financial Year Income Tax Rates (Data Source: ATO)

| Tax Type | Taxpayer | Taxable Event | Tax Calculation Principle | Specific Tax Calculation Rules |

|---|---|---|---|---|

| Capital Gains Tax | Investor | Selling cryptocurrency for fiat currency | Capital Gain = Sales Price (Market Value) - Cost Base | Calculate the capital gain based on the market value of the crypto asset. |

| Gifting cryptocurrency | Calculate the capital gain based on the market value of the crypto asset. If it is a gift to an organization with Deductible Gift Recipient (DGR) status, and it is a testamentary gift, under a cultural bequest program, or a personal use crypto asset, no capital gains tax is required. | |||

| Exchanging using cryptocurrency | When exchanging old crypto assets for new crypto assets, calculate the capital gain based on the market value of the new crypto assets. If the value of the new crypto assets obtained in the crypto asset exchange or swap cannot be determined, the market value of the old crypto assets can be used to calculate the capital gain. | |||

| Purchasing goods or services with cryptocurrency | Calculate the capital gain based on the market value of the crypto asset. | |||

| Ordinary Income Tax | Trader | Mining | Treated as ordinary income under standard income tax rules | If acting as an amateur miner, receiving mining rewards requires no tax payment. If mining as a corporate employee, the value of the coins at the time of mining is deemed ordinary income and is taxed at the marginal tax rate. |

| Staking | The additional tokens obtained are ordinary income; declare this income as other income when filing taxes. | |||

| Airdrops | The monetary value of established tokens obtained is ordinary income; declare this income as other income when filing taxes. If the token is untraded prior to the airdrop, it is deemed an initial allocation airdrop and is tax-free upon receipt. | |||

| Remuneration payments | When receiving crypto assets as payment for employment or services, this payment must be treated as assessable income, recording the market value calculated in Australian Dollars (AUD). | |||

| No Tax Required | / | Purchasing cryptocurrency using Australian Dollars or other currencies | / | / |

| Transferring between one's own wallets | ||||

| Merely holding cryptocurrency without disposal |

Table 2. Specific Tax Treatment Scenarios for Crypto Assets in Australia

Under current tax laws, the ATO has provided relevant guidance on tax compliance issues for emerging scenarios such as DeFi and NFTs.

DeFi protocols commonly use traditional financial terminology to describe their products, such as lending, borrowing, and interest. However, these activities within DeFi protocols do not always reflect their conventional meanings and tax purposes. The essential difference between them and traditional finance lies in whether the asset has been disposed of or rights have been exchanged, no longer being controlled by the original owner, thereby triggering capital gains tax. Therefore, the ATO determines whether capital gains tax is triggered based on whether control is lost, whether a new asset or right is acquired, and whether a change in beneficial ownership has occurred. Meanwhile, rewards or yields generated by DeFi protocols are typically identified as ordinary income, processed according to ordinary income tax rules.

As a blockchain-based digital asset credential, an NFT itself can represent ownership of any tangible or intangible asset. Therefore, the ATO judges whether it belongs to the capital gains tax track or the ordinary income tax track according to the user entity, holding purpose, and trading method. If an NFT is used for investment purposes or as an enterprise capital asset, capital gains tax rules apply. If an NFT is used for operational or commercial purposes, ordinary income tax rules apply. If an individual uses an NFT solely for personal consumption or entertainment, it is identified as a personal use asset.

However, the ATO itself acknowledges that its income tax position on cryptocurrency yields is still in dynamic evolution, and it continuously updates guidance on emerging scenarios such as DeFi yields, staking rewards, airdrops, and NFT transactions. Current guidance fails to completely cover the tax treatment issues of emerging scenarios. For example, NFT rewards obtained through games are preliminarily identified as ordinary income, but whether subsequent operations such as trading, upgrading, and synthesizing of in-game NFTs trigger capital gains tax, and how the boundary between game props and NFTs is delineated, all await further clarification.

The Self-Managed Superannuation Fund (SMSF) is a unique retirement savings institutional arrangement in Australia, occupying about a quarter of the market share in the Australian superannuation market. Holding crypto assets through an SMSF is not prohibited by regulation, but the applicable framework includes both significant tax concessions and notably higher compliance thresholds superimposed compared to general taxpayers.

From the perspective of tax treatment, an SMSF holding crypto assets has not departed from existing CGT rules, but embeds the unique concessional tax rate structure of SMSFs. Specifically: the fund's taxable income is levied at a concessional tax rate of 15%; upon disposal, if the holding period exceeds 12 months, a 1/3 CGT discount can be applied, and the effective tax rate for long-term capital gains is approximately 10%; when the fund enters the pension payment phase, the relevant yields supporting current pension liabilities can enjoy a zero tax rate.

But the concessional tax structure comes at a price, manifested in strict compliance requirements:

First, investment eligibility. Crypto asset investments must be explicitly permitted in the fund's trust deed, and the investment strategy must make specialized written considerations regarding the volatility and liquidity of crypto assets, as well as their alignment with members' retirement objectives. Among these, the sole purpose test is the underlying principle—all investment behaviors of the fund must serve the sole purpose of providing retirement benefits for its members.

Second, asset segregation. Crypto assets held by the fund must be custodied in independent wallets in the name of the SMSF, strictly separated from the personal crypto assets of the trustee or members; exchange accounts and hardware wallets must all be registered in the fund's name. The fund is also not allowed to acquire crypto assets from a related party, because crypto assets are not on the related party acquisition exception list (which only contains listed securities, commercial real estate, etc.) of the Superannuation Industry (Supervision) Act (SIS Act).

Third, valuation and auditing. Crypto assets must be valued according to the market price on June 30 each year and reflected in the fund's financial statements; exchange bills or position screenshots alone do not constitute sufficient valuation evidence; licensed SMSF auditors must conduct independent verification of the ownership, existence, and valuation of the fund's crypto assets every year.

Fourth, non-compliance consequences. If identified as a non-complying fund, all its assets will be taxed at the highest marginal tax rate (currently 45%), the tax concessions enjoyed will be clawed back all at once, and it possesses irreversibility.

In specific practice, the tax treatment of crypto assets may face even more complex special scenarios. These scenarios usually involve multiple legal relationships or institutional objectives, thereby putting forward higher requirements for the interpretation and application of existing tax law rules.

In summary, Australia did not establish a new set of dedicated systems for crypto assets, but embedded crypto assets under the existing tax and regulatory frameworks. This exempted lengthy legislative procedures and institution-building processes, maintaining the stability and continuity of the existing framework, but it also led to the issue of relatively large elastic interpretation space of existing rules in special scenarios and the existence of partial institutional blanks, increasing compliance costs and legal uncertainty.

The compliance focuses of different types of market participants vary. For individual investors, the core lies in accurately identifying taxable events and standardizing the recording of transaction data to avoid underestimating tax obligations. For high-frequency traders or entities with an operational nature, key attention must be paid to the boundary between investment and business activities to ensure that tax characterization aligns with the actual business model. For platforms and service providers, their compliance responsibilities are not limited to their own tax obligations, but may also extend to information reporting, customer identification, and transaction transparency.

Looking ahead, in the process of realizing regulatory unification, Australia may further refine the digital asset classification and service provider licensing system, to comprehensively cover various forms of digital assets, and strengthen articulation with international rules, thereby attracting institutional participants of more complex tiers to enter.

FinTax offers crypto accounting suite, tax calculator and professional tax consulting services.