In 2026, a noteworthy divergence has emerged within the crypto industry.

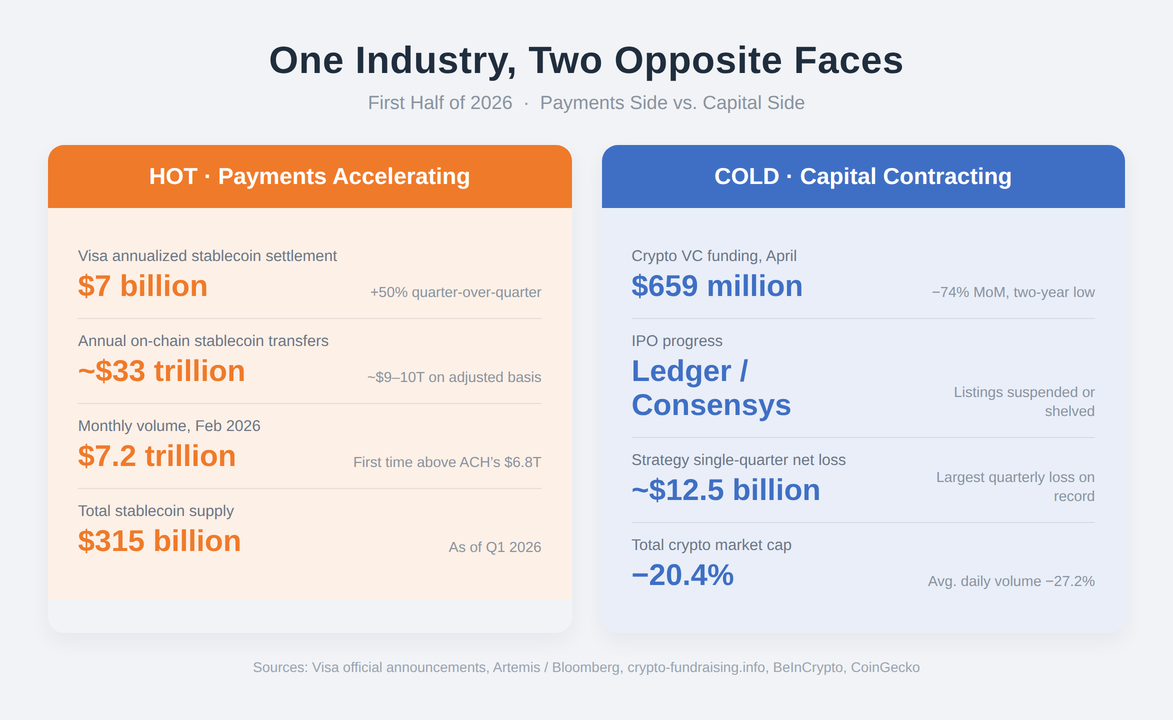

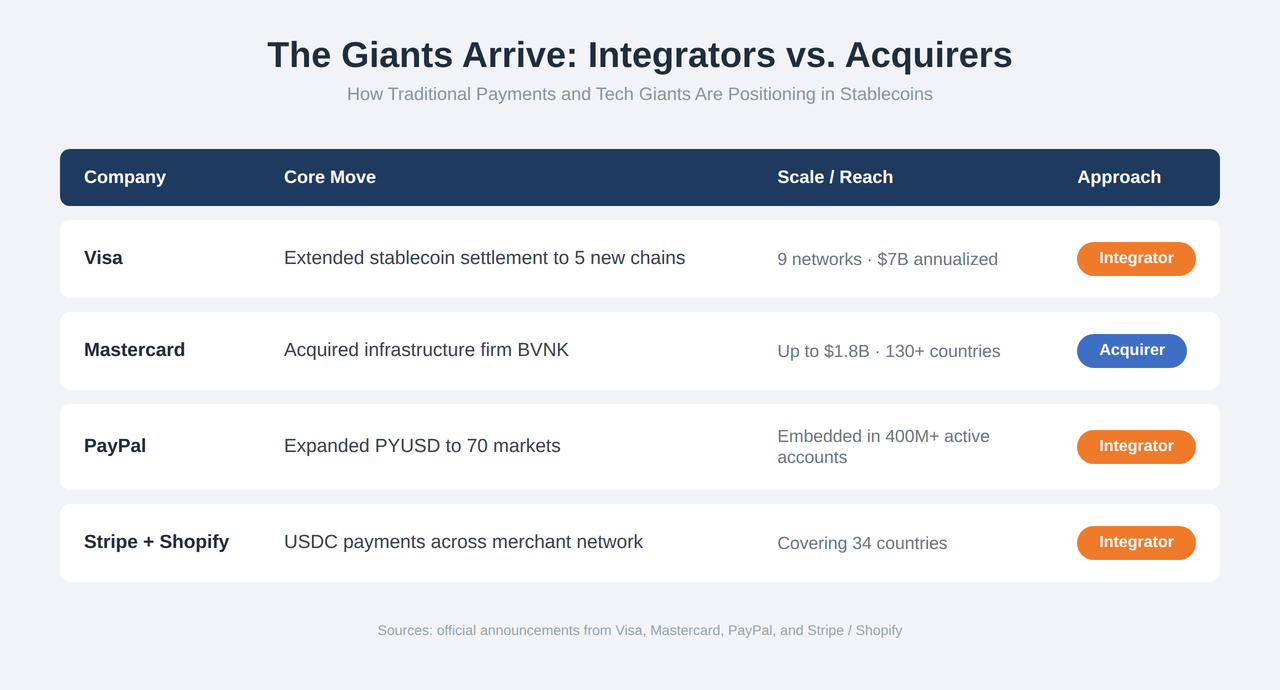

On one side, the payments business is racing ahead. On April 29, global payments giant Visa announced it would extend its stablecoin settlement pilot to five more blockchains—Arc, Base, Canton, Polygon, and Tempo—raising the number of supported settlement networks from four to nine. On May 5, Visa partnered with Canadian financial platform Wealthsimple, bringing the stablecoin settlement pilot to the Canadian market for the first time. As the issuer behind billions of cards worldwide, Visa’s move into on-chain settlement signals its endorsement of the value of stablecoin payments.

On the other side, the capital business is stalling. In May, French hardware-wallet maker Ledger suspended its U.S. IPO plans, which had carried a valuation of more than $4 billion, while Ethereum application developer Consensys also shelved its own listing. The performance of already-listed crypto firms is hardly encouraging either: since its IPO, Circle has seen its USDC stablecoin business markedly affected by swings in market interest rates; and although eToro set new records for net profit and funded accounts in Q1 2026, its crypto-asset revenue fell 38% year-over-year and its net crypto-derivatives trading revenue dropped 57%.

These two phenomena may look unrelated, but together they reflect a structural realignment of where capital and business focus sit within the crypto market: the practical adoption of payment infrastructure is accelerating, even as valuations and fundraising in the capital markets contract. Within the same industry and over the same period, why are the payments side and the capital side moving in opposite directions? And following this logic of divergence, where might the crypto market be headed next?

Before asking why, we first need a rough sense of what is being compared. From on-chain payments to IPOs, the scale and direction of each side already tell us a great deal.

On-chain stablecoin activity has now reached a substantial scale. In headline terms, stablecoin on-chain transfer volume totaled roughly $33 trillion across 2025—a figure that even exceeded Visa’s total payments volume of about $16.7 trillion over the same period. After adjustments by firms such as Artemis and Visa that strip out non-economic activity such as market-making bots and intra-exchange transfers, genuine on-chain economic transfers in stablecoins came to roughly $9–10 trillion.

The monthly figures point to the same acceleration. In February 2026, monthly stablecoin transaction volume reached $7.2 trillion, surpassing the $6.8 trillion handled by the U.S. ACH (Automated Clearing House) network for the first time. By Q1 2026, the total stablecoin supply had reached $315 billion. Visa’s $7 billion is a small share of this vast market, but it represents institutional-grade settlement processed through a compliant card-network and directed at issuing and acquiring institutions—not retail transfers on-chain. Beyond that, as traditional payment giants such as Visa and PayPal connect to stablecoin payments, they bring with them a wealth of supporting infrastructure, including settlement networks, that sharply lowers the barrier for businesses and ordinary users to use stablecoins. When a cross-border e-commerce merchant can enable USDC payments on Shopify with a single click and have them settled automatically into fiat via Visa, stablecoins become one of the payment options available to that merchant. In this sense, stablecoin settlement is gradually being absorbed into the traditional payment system.

In contrast to the accelerating growth of stablecoin payments, the capital side is under strain—visible across fundraising, valuations, and investment logic alike.

In the primary market, total crypto VC funding in April 2026 came to roughly $1.554 billion, down 66.91% from March’s $4.696 billion and 42.75% lower year-over-year. Both deal frequency and average check size are falling in tandem, with capital concentrating further in a handful of leading projects and early-stage fundraising growing harder. In Q1, prediction-market platforms Kalshi and Polymarket closed mega-rounds of $1 billion and $600 million respectively, and together with Mastercard’s $1.8 billion acquisition of BVNK, these three deals alone accounted for nearly half of the capital disclosed that quarter. The picture for early-stage projects stands in sharp contrast: seed-round deal count for the quarter was down more than 60% from its 2022 peak, the median seed round fell below $2 million, and seed and earlier-stage rounds combined made up only about 5% of total VC funding. Compared with the 2021–2022 mindset that “a sector alone was enough to justify a valuation” and the indiscriminate, scatter-shot funding it produced, institutions today are more inclined to bet on directions whose market prospects have already been validated, and the funding environment for long-tail projects has tightened noticeably.

In the secondary market, setting aside Ledger and Consensys, whose listings are on hold, the crypto firms that have completed IPOs also broadly face the challenge of valuation repricing, tightly bound to token-price movements. Take Strategy (formerly MicroStrategy): as the public company with the largest bitcoin holdings, it recorded a net loss of roughly $12.5 billion in Q1 2026—its largest single-quarter loss on record—driven mainly by mark-to-market writedowns on those holdings. Strategy’s share price fell about 27% between January and June this year, with an even steeper decline over the past twelve months. Leading crypto exchange Coinbase has come under heavy pressure as well: Q1 revenue of $1.41 billion missed market expectations, trading revenue fell about 23% quarter-over-quarter, and its share price was down more than 20% at one point during the year. The high volatility in both firms’ revenue and earnings is a clear reflection of the cooling sentiment on the capital side.

Finally, on investment logic, the yardsticks institutions apply to crypto firms have shifted from scale metrics such as trading volume and user growth toward fundamentals such as cash-flow quality, revenue mix, and compliance costs. Yet as of Q1 2026, total crypto market cap had fallen 20.4%, average daily trading volume was down 27.2% quarter-over-quarter, and a number of crypto-related stocks had broken below their issue price by more than 30% after listing—developments that clearly weaken the pricing power and the appetite for future crypto IPOs, which in turn drags down liquidity and sentiment in the secondary market in lockstep. Capital’s metrics for pricing crypto firms have grown more grounded, but the market environment has failed to meet those expectations.

Why are these two directions in today’s crypto market diverging so visibly? The key to answering this is to clear up a common misconception: within crypto, the payments side and the capital side were never driven by the same force, and the two are not in a trade-off where one rises as the other falls.

Visa’s deeper push into stablecoin settlement is one snapshot of the organic growth within the crypto payments segment. Why can crypto payments keep growing even as the broader industry cools? First, there is demand: long-standing pain points in the traditional cross-border payment system form the bedrock of crypto payments. Second, there is supply: the collective entry of traditional payment giants and crypto-native firms is accelerating the buildout of this segment’s infrastructure and reshaping everyday spending habits.

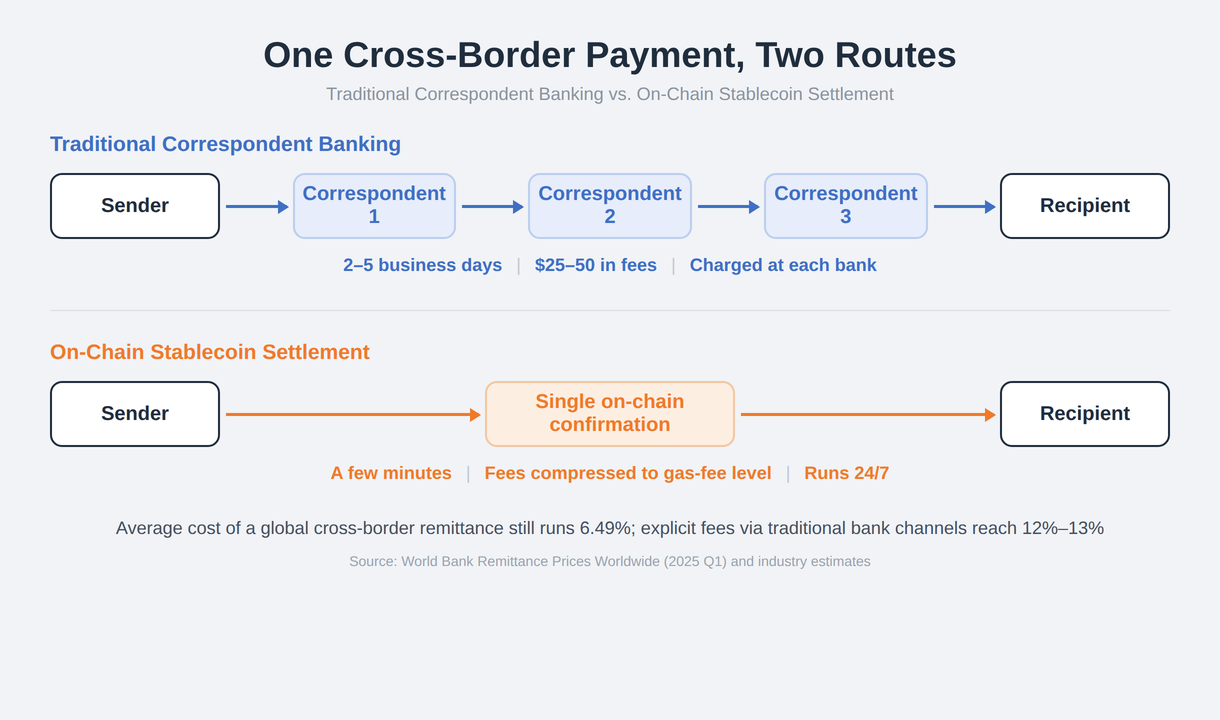

On the demand side, cross-border economic activity depends heavily on low-friction payment networks, yet the traditional correspondent-banking model has a long clearing chain and a tangle of compliance checkpoints, making a more efficient and more economical cross-border payment tool a shared goal for everyone. In Q1 2025, the average cost of a global cross-border remittance still ran as high as 6.49%—far above the 3% target set by the UN Sustainable Development Goals—with explicit fees through traditional bank channels averaging 12% to 13%. B2B cross-border transfers cost even more: a typical transfer passes through three to five correspondent banks, takes two to five business days, carries fees of $25 to $50, and is charged at each intermediary bank along the way. The value of stablecoin settlement lies precisely in bypassing this multi-layered system—funds are confirmed once on-chain, and fees are compressed to roughly the level of a gas fee. At the same time, a network running 24/7 is not bound by bank business hours, so cross-border fund transfers can be completed within minutes. These advantages make stablecoin settlement an emerging option for cross-border settlement.

For most people, the need for a low-friction cross-border payment network is enduring and independent of the token-price cycle: whether bitcoin rises or falls, traders still need to remit funds and exporters still need to convert foreign exchange—and this is the fundamental reason the payments segment can stay decoupled from sentiment in the crypto capital markets.

On the supply side of crypto payments, the maturity of the infrastructure reached an inflection point in 2025–2026. Before 2023, the rollout of stablecoin payments was held back by poor on- and off-ramp channels and inconsistent compliance standards. By 2025 and 2026, however, the arrival of payment infrastructure such as Circle’s Cross-Chain Transfer Protocol (CCTP), the embedded wallets of PayPal and Stripe, and Visa’s stablecoin settlement network has lowered the barrier for businesses and ordinary users to use stablecoins. In March 2026, PayPal extended its dollar stablecoin PYUSD to 70 markets worldwide, embedding stablecoins into the ready-made interface of more than 400 million active accounts. That same month, Mastercard announced it would acquire stablecoin infrastructure company BVNK for up to $1.8 billion (including $300 million in contingent consideration); BVNK operates in more than 130 countries and is licensed across multiple jurisdictions. Stripe and Shopify, meanwhile, have brought stablecoin payments directly to merchants and consumers, rolling out USDC payments across a global merchant network spanning 34 countries since June 2025. When a cross-border e-commerce merchant can enable USDC payments on Shopify with a single click and have them settled automatically into fiat via Visa, stablecoins become one of the payment options available to that merchant. Falling market-education costs and lower barriers to entry are an essential precondition for payments to scale.

The slump in crypto IPOs and VC funding follows a different logic, one woven from dependence on token prices, doubts about business models, and steadily rising compliance costs. The first factor is heavy dependence on crypto-asset prices. The firms suspending or postponing their listings are concentrated in exchanges, miners, wallets, and infrastructure—businesses whose revenue is highly sensitive to market trading volume and price. When total market cap keeps falling and average daily trading volume undershoots expectations, these firms’ revenue forecasts and valuation ranges are pushed down directly, and the IPO window narrows accordingly. Second, doubts about the sustainability of crypto business models are building. The core revenue of listed firms such as Coinbase and BitGo still leans heavily on trading fees and custody fees, lacking a diversified revenue mix. As narratives such as trade mining and staking yields recede, investors have begun to scrutinize these firms with stricter discounted-cash-flow models, while the post-IPO breaks below issue price among several crypto-related stocks have further eroded pricing power for subsequent listings.

Finally, the accelerating arrival of regulatory frameworks is raising the compliance bar and reshaping firms’ cost structures. On one hand, the tax-transparency framework has entered the operational phase: under the OECD’s Crypto-Asset Reporting Framework (CARF), the first cross-border information exchanges will begin in 2027, with crypto-asset service providers such as exchanges, wallets, and brokers broadly designated as reporting entities required to collect and report users’ tax-residency status and transaction data. On the other hand, licensing and issuance rules across major markets are gradually taking shape: the U.S. GENIUS Act has established a federal framework for stablecoins, and jurisdictions such as Hong Kong and the UAE have rolled out licensing regimes one after another. In this environment, crypto firms’ compliance spending—on KYC/AML system overhauls, data reporting, and license applications and maintenance—will become a fixed cost that directly compresses profit margins. For institutional investors, crypto firms’ steadily rising compliance costs are a factor hard to ignore before making an investment decision.

Placing the two threads side by side makes the logic of the divergence clear. The cooling of crypto IPOs reflects speculative capital retreating from high-risk narratives, while the heating of crypto payments reflects productive capital adopting an efficiency tool. Their driving forces differ, which is why their trajectories visibly diverge. That Visa is willing to commit real money during a crypto winter says something in itself about its confidence in long-term demand; the scale is still that of a pilot, but this is voting with capital rather than a partnership that exists only on slides.

At the same time, the capital markets’ valuation of crypto firms is shifting toward a greater focus on cash flow: within the same quarter, names backed by stable settlement cash flows held up relatively well, while pure-narrative stocks reliant on a trading-volume story fared worse. This shows that the pricing logic in the crypto market has already diverged—and rather than a downturn, this divergence is better understood as the return to fundamentals it ought to be. The market is no longer paying a premium for the narrative that “things will get better,” and is beginning to focus more on the utility that is visible right now.

The sustained momentum in crypto payments is driven by the real economy’s genuine need for a more efficient cross-border payment system, while the simultaneous pressure on crypto IPOs and VC funding reflects the broad predicament of asset-driven segments amid swings in the token-price cycle. Across the industry as a whole, the crypto market is undergoing a divergence that comes with gradual maturation—business segments close to real demand that generate steady utility, and those that hinge on price expectations and high volatility, are now tracing markedly different paths. From this starting point, the future of the crypto market could unfold in several directions:

First, stablecoins continue to move from the crypto world into the traditional payment system, complementing it. The Bank for International Settlements has noted that tokenizing central-bank reserves and commercial-bank deposits could significantly improve cross-border payment efficiency. That said, the main engine of future growth will be inelastic, non-cyclical demand such as B2B and cross-border remittances, rather than retail speculation.

Second, compliance is likely to become a watershed that splits the market into two layers: one of licensed stablecoins, serving institutions and cross-border settlement and plugging into card networks and the banking system; and another of offshore, freely circulating stablecoins, handling retail and peer-to-peer transfers in emerging markets. As the mainstream rails grow increasingly compliant, the network effects of the former will compound, the difficulty of plugging the latter into mainstream commercial systems will keep rising, and the room for regulatory arbitrage will continue to narrow.

Third, the division of labor between giants and startups will become further entrenched, and a contest between two approaches may emerge. One is the Visa-style “integrator” approach, keeping stablecoin flows within its existing global network; the other is the Mastercard-style “acquirer” approach, buying the entire compliant technology stack outright. Whichever path prevails, giants will lay the standardized rails while startups do deep customization by region, use case, and industry. And for startups that try to take on the giants head-to-head on infrastructure, survival will only get harder.

Returning to the original question: payments racing ahead while capital pulls back is not a cause-and-effect relationship but the real-world expression of different segments within the same industry diverging. Businesses close to real demand that generate steady utility, and businesses that hinge on price expectations and high volatility, are tracing markedly different paths; and the crypto industry’s shift from blanket hype to segment-level divergence is itself one of the markers of its maturation. As for the future, whether stablecoins can truly become a complementary layer of the global payment system will depend on sustained validation—of regulatory coordination, technical interoperability, and business models—over the next three to five years. How well these questions are answered will determine whether they end up as the niche payment instrument the BIS describes, or genuinely constitute a layer of the payment system. For the crypto market, the certainty of its development is increasing, but the regulatory environment remains the single most critical variable.

FinTax offers crypto accounting suite, tax calculator and professional tax consulting services.